I Want to Buy a Home

I Want to Refinance

Search For a Loan Officer

-

NAME

-

Location

Focus on Your Home Experience

We’ll focus on your Loan Experience

Calculate Your Monthly Payment

Monthly Payment Calculator

Your monthly mortgage payment is calculated by adding the costs of the loan’s principal and interest, as well as any money held in escrow for taxes and insurance. How much will it be? Get an idea now and compare different loan terms.

The answers to all your mortgage questions...

Committed to giving you all the support and guidance you need to find the right mortgage options for you and your family.

About Us

OUR STORY

OUR STORY

OUR

BRANCHES

OUR

BRANCHES

CAREERS

CAREERSOur Story

For more than ten years, Homefront Mortgage has provided industry-leading mortgage services and helped countless homebuyers and homeowners find financing solutions to meet their needs. Our reputation is based on building and maintaining relationships that last long after you get the keys to your home.

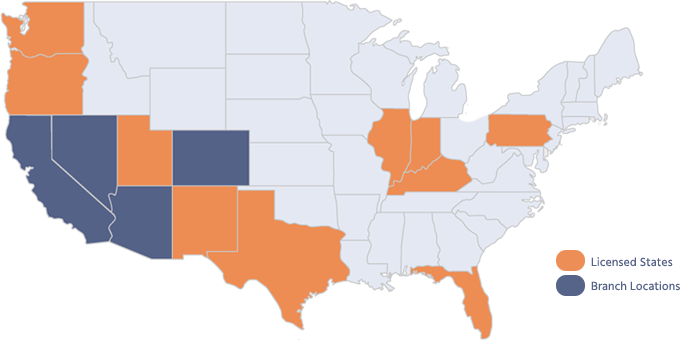

Branch Locations

When it comes to your home, no question is too big or

too small for

our Loan Officers

Together, we can find your happy place!